UK banks can increase riskier mortgage lending, BoE says

Newsflash: The Bank of England is recommending that lending rules are relaxed so that banks and building societies can issue more mortgages at high loan-to-income levels.

The BoE’s Financial Policy Committee is recommending that individual lenders should be allowed to increase their share of lending at high LTIs to above the current limit of 15%.

This could make it easier for borrowers to stretch themselves to afford a more expensive property.

High loan-to-income loans are defined as those at a ratio above 4.5. Loans above this level are riskier, as borrowers could struggle to meet mortgage payments if their incomes fell, or if interest rates rose.

Announcing the plan, the FPC says:

The Committee noted its role in supporting the Government’s priority to make home ownership more accessible and discussed the UK housing market and the role of regulatory mortgage policies.

It wants the overall lending market to restrict high LTI loans to 15% of total demand, while allowing individual lenders to exceed it. The loan-to-income lending limit was introduced in 2014, as part of a package to cool the housing market.

The FPC says:

The Committee noted that the original policy intent of the LTI flow limit recommendation was to ensure the flow of new residential mortgages at high LTIs did not exceed 15% of total new mortgages in aggregate.

The FPC judged that the aggregate 15 per cent limit continued to strike the right balance between providing appropriate protection from the increased risk to economic growth of large cuts to consumption associated with an over-indebted household sector, while providing sufficient capacity for otherwise creditworthy households to borrow at higher LTIs.

As such, it has recommended the Prudential Regulation Authority (PRA) and the FCA amend implementation of its LTI flow limit to allow individual lenders to increase their share of lending at high LTIs while aiming to ensure the aggregate flow remained consistent with the limit of 15%.

Key events Show key events only Please turn on JavaScript to use this feature

BoE governor opposes forcing pension funds to invest in UK

BoE governor Andrew Bailey then calls for reforms to the UK pension system, but opposes the suggestion that funds should be forced to buy UK assets.

Q: what’s your view on the possibility that the government will mandate how much invest pension funds should invest in UK assets?

Bailey replies that the UK only has a low level of pension fund investment in “the real economy in this country”, and that structural changes to the pension fund industry (consolidating funds) would be helpful.

However, he says:

I do not support mandating. I don’t think that’s appropriate.

He adds that the current government is taking the same approach as its predecessor on this issue, adding

I think reforming the pension system does, to be honest, require a lot of heavy lifting, but it needs to be done.

It will take a bit of time, but it needs to be done for these structural reasons. I don’t support mandating, but I do hope that we can reach a point where there is a natural ability to tackle this problem.

Earlier this year, chancellor Rachel Reeves said she would create a “backstop” power to force large pension funds to back British assets, if necessary, to drive up investment.

Bailey: economic fragmentation bad for activity and employment

Q: Will a global trade war lead to UK job losses?

BoE governor Bailey replies that there’s been a big increase in uncertainty around trade and tariffs, pointing out:

Fragmenting the world economy is bad for activity in the world economy. That’s fairly simple trade theory.

That fragmentation is bad for economic activity, and is therefore bad for employment, he adds:

“Obviously, in that sense, there is a consequence. So we have to watch that very carefully.”

Bailey adds that it was a “very good thing” that the UK government was first to negotiate a trade agreement with the US.

Q: Your report warns that a weak IPO market is resulting in fewer exit opportunities for private equity backed firms. How concerned are you about the lack of buoyant public markets, including in London? (my colleague Kalyeena Makortoff asks).

BoE governor Andrew Bailey replies that firms are telling the Bank that they are delaying investment decisions due to the higher level of uncertainty in the world economy. That can include decisiont on whether to raise capital, and in which market to raise it.

Bailey adds:

It’s not surprising, because economics and economic theory tells us this, that since investment decisions are typically irreversible. Once you take them, once you start them, you’ve got to go on, as it were. You usually can’t turn back.

Then if uncertainty increases, then the option value of delaying goes up. And so you do see delayed investment, and I think we are seeing that at the moment.

Bailey: Rise in UK bond yields part of global move

Q: What does the bond market reaction to the chancellor’s tears (last week) say about the fragility of the bond market?

Andrew Bailey replies that there have been “broadly similar” movements in global government bond markets.

Bailey says:

We’ve seen steepening of yield curves globally. So I think it’s important to start in that context. There’s nothing, I would say, particularly UK focused about that. That steepening pattern is a global trend which the UK market has been part of.

Bailey points out that the rise in UK bond yields last week did reverse (they fell back after Keir Starmer backed chancellor Rachel Reeves, easing concerns of a change of chancellor).

That, he adds, is further evidence that we are in a period of more volatile markets, and one where there is also “fast reversion”.

Andrew Bailey then explains that the BoE is putting its recommendation that lenders should offer more high loan-to-income mortgages into place from today.

BoE governor Andrew Bailey then warns that another bout of trade war market turbulence could hurt the UK economy.

He reminds reporters in London about the market slump in early April after Donald Trump announced new tariffs, in which risky asset prices fell and the US dollar weakened.

Bailey says core government bond markets remained orderly during this stressful period, but warns that conditions might have become more strained if the episode of volatility had lasted for longer.

Risk sentiment in some markets then recovered after president Trump paused these tariffs, Bailey reminds us – before warning that the risksk of another selloff remain high.

He says:

There has been a notable change in the usual correlation patterns between the dollar and other US assets, including equities and government bond yields.

And given these developments, the risk of sharp falls in risky asset prices, abrupt shifts in asset allocation and a more prolonged breakdown in historical correlations remains high, and vulnerabilities in market based finance could amplify such moves which could impact the availability and cost of credit here in the UK.

BoE's Bailey: geopolitical, trade and sovereign debt risks still high

Bank of England governor Andrew Bailey has warned that the UK is particularly exposed to geopolitical risks, as it is an open economy with a large financial sector.

Briefing journalists in London about today’s financial stability report, he says:

Risks and uncertainty associated with geopolitical tensions, global fragmentation of trade and financial markets and pressures on sovereign debt markets are still elevated.

Some geopolitical risks have crystallized and material uncertainty around the global macroeconomic outlook persists.

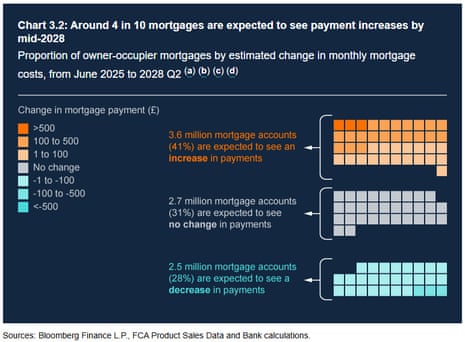

Millions more face mortgage timebomb

The Bank of England is also warning that over three and half million mortgage holders are on track to pay higher payments by 2028.

That’s because around 30% of mortgage holders have not yet refixed their mortage deals since interest rates started to rise at the end of 2021.

This means the full impact of higher interest rates has not yet passed through to all mortgagors, the Bank says.

However, another 2.5 mortgage holders can look forward to a drop in payments. That’s because rates peaked at 5.25% in August 2023 and were held for 12 months, followed by four quarter-point cuts over the last year.

BoE: US tariffs will weigh on world growth

Donald Trump’s trade war has created uncertainty that will hurt growth in the global economy, the Bank of England warns.

It’s new Financial Stability Report (FRS) also singles out the Middle East crisis as a factor making it hard to forecast inflation.

The BoE says:

Since the November FSR, the US announced increased tariffs, and in response some other jurisdictions announced changes to their own trade policies. Negotiations between the US and China led to a partial reversal of tariff increases in May, with further agreement subsequently reached, and a trade deal has been agreed between the US and the UK. There remains, however, considerable unpredictability about the near-term evolution of global trade policies with negotiations continuing between the US and a number of its trading partners.

These developments are expected to weigh on world growth, driven both by the direct impact of higher tariff barriers and by the dampening effect of trade policy uncertainty on firms’ investment decisions.

There is a high degree of economic uncertainty around the outlook, and there are downside risks to global growth in the near term, for example in the event of significant global supply chain disruption or further escalation of conflict in the Middle East leading to higher energy prices. These factors also contribute to uncertainty around the future path of inflation.

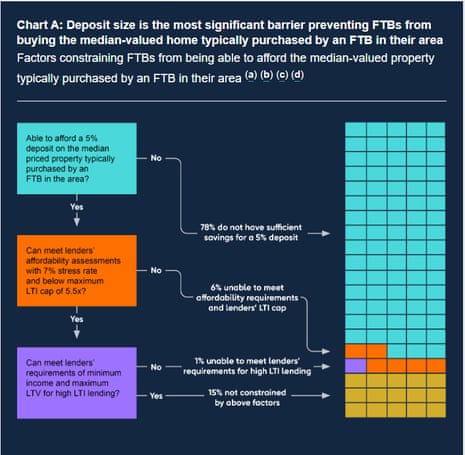

BoE: accumulating a deposit is main barrier to owning a home

The Bank of England’s financial policy committee also points out that accumulating a sufficient deposit continues to be the main barrier to owning a home.

Its new financial stability report, just released, shows that almost 80% of prospective first-time buyers (FTB) do not have sufficient savings to cover a 5% deposit on a median-priced property typically purchased by an FTB in their area.

Another 6% are restrained by lenders’ affordability assessments, and loan to income (LTI) ratio caps.

A further 1% would not meet other requirements lenders set to manage their high-LTI lending (such as rules around minimum salary), leaving just 15% of prospective first-time buyers who can actually (potentially) buy a typical appropriate property in their area!

UK banks can increase riskier mortgage lending, BoE says

Newsflash: The Bank of England is recommending that lending rules are relaxed so that banks and building societies can issue more mortgages at high loan-to-income levels.

The BoE’s Financial Policy Committee is recommending that individual lenders should be allowed to increase their share of lending at high LTIs to above the current limit of 15%.

This could make it easier for borrowers to stretch themselves to afford a more expensive property.

High loan-to-income loans are defined as those at a ratio above 4.5. Loans above this level are riskier, as borrowers could struggle to meet mortgage payments if their incomes fell, or if interest rates rose.

Announcing the plan, the FPC says:

The Committee noted its role in supporting the Government’s priority to make home ownership more accessible and discussed the UK housing market and the role of regulatory mortgage policies.

It wants the overall lending market to restrict high LTI loans to 15% of total demand, while allowing individual lenders to exceed it. The loan-to-income lending limit was introduced in 2014, as part of a package to cool the housing market.

The FPC says:

The Committee noted that the original policy intent of the LTI flow limit recommendation was to ensure the flow of new residential mortgages at high LTIs did not exceed 15% of total new mortgages in aggregate.

The FPC judged that the aggregate 15 per cent limit continued to strike the right balance between providing appropriate protection from the increased risk to economic growth of large cuts to consumption associated with an over-indebted household sector, while providing sufficient capacity for otherwise creditworthy households to borrow at higher LTIs.

As such, it has recommended the Prudential Regulation Authority (PRA) and the FCA amend implementation of its LTI flow limit to allow individual lenders to increase their share of lending at high LTIs while aiming to ensure the aggregate flow remained consistent with the limit of 15%.

Here’s our news story about the jump in the US copper price:

The oil price has hit its highest level in two weeks, after a cargo ship attacked in the Red Sea sank.

The Eternity C cargo ship sank in the Red Sea following an attack on Monday, blamed on Yemen-Houthi militants, which killed at least four crew members.

Brent crude has risen by 0.6% today to $70.71 per barrel, the highest since 23 June.

Tom Bailey, head of research at HANetf, has warned that the threat of copper tariffs is leading to more of the metal becoming ‘trapped’ in warehouses, rather than being used.

Bailey explains that this could distort prices for this vital metal:

Copper sits at the centre of a looming supply-demand crunch. On one side is surging demand driven by grid upgrades, the rapid buildout of AI data centres, and the ongoing urbanisation of emerging markets. On the other is a supply base that is ageing, expensive, and increasingly unreliable. Ore grades are declining, discoveries are rare, and new mines take over a decade to come online.

“However, tariffs mean that a new dynamic is potentially emerging: trapped copper. With tariffs looming, US buyers have rushed to bring in copper ahead of schedule. But much of this metal is not being consumed. Instead, it is sitting in warehouses or locked in financing agreements. Due to high US premiums, it is uneconomical to export. In practice, this copper is being stranded inside the US, unavailable to the rest of the world.

The result could be distorted physical markets, with those outside the US forced to compete for a shrinking pool of freely available copper.

German chancellor Friedrich Merz is optimistic that the European Union can agree a trade deal with the United States by the end of this month at the latest.

Merz told lawmakers on Wednesday:

“Our goal is to reach a trade agreement with the United States of America as quickly as possible that links mutual trade between America and the European Union with the lowest possible customs duties.”

Merz added that he is in close contact with US president Donald Trump and the European Commission.

Shares in some European pharma companies have dropped this morningn, after Donald Trump threatened to implement up to 200% tariffs on imported pharmaceuticals.

The falls are modest, though, after Trump also said he would give drugmakers about one year “to get their act together”.

In London, AstraZeneca’s shares have dipped by 0.77%.

Switzerland’s Novartis has lost 0.8%, while Belgium’s UCB has dropped by 1.75%.

Dan Coatsworth, investment analyst at AJ Bell, says:

“The pressure is now on for drug companies to expand US production facilities so they are effectively on the doorstep of American customers. Boosting the manufacturing sector and creating more jobs is central to Trump’s tariff strategy, and the likes of AstraZeneca already have plans in motion to expand their US footprint.